There’s something a little weird about short selling. Shorting—or betting that a stock’s price will fall—is a feature of finance that doesn’t have a close analogue in the real-world economy.

Buying a stock you like isn’t much different from purchasing a product that catches your eye. But if you’re walking through the local grocery store and see an item that sets your stomach turning—say, ketchup-flavored potato chips—you don’t stand in the aisle waving off other customers, telling them how bad it is. You don’t try to crush the bag. You just think, “Who in the world eats this … ” and go on your merry way without putting it in your cart.

On the stock market, you can do more than just ignore the stuff you think is lousy. You can actively hunt down weak companies or overpriced stocks and try to profit from their decline. Shorting is an old practice—Napoleon outlawed it—that’s become a taken-for-granted part of modern finance. Hedge funds couldn’t hedge without some form of shorting; it’s a kind of insurance that something in a portfolio is making money even if the market falls.

And right now a lot of people hate it. A common thread among many of the stocks retail investors have embraced—including GameStop Corp. and AMC Entertainment Holdings Inc.—is that they’ve also been targeted by short sellers. The traders who call themselves “apes” on Twitter and Reddit discussion boards see themselves as an army at war with the short sellers from elite Wall Street.

In fact, fans of these so-called meme stocks are locked into a symbiotic relationship with the shorts. Part of the reason GameStop and AMC were launched to the moon is that a frenzied group of traders thought they had an opportunity to make money by overpowering the short bets placed by hedge funds.

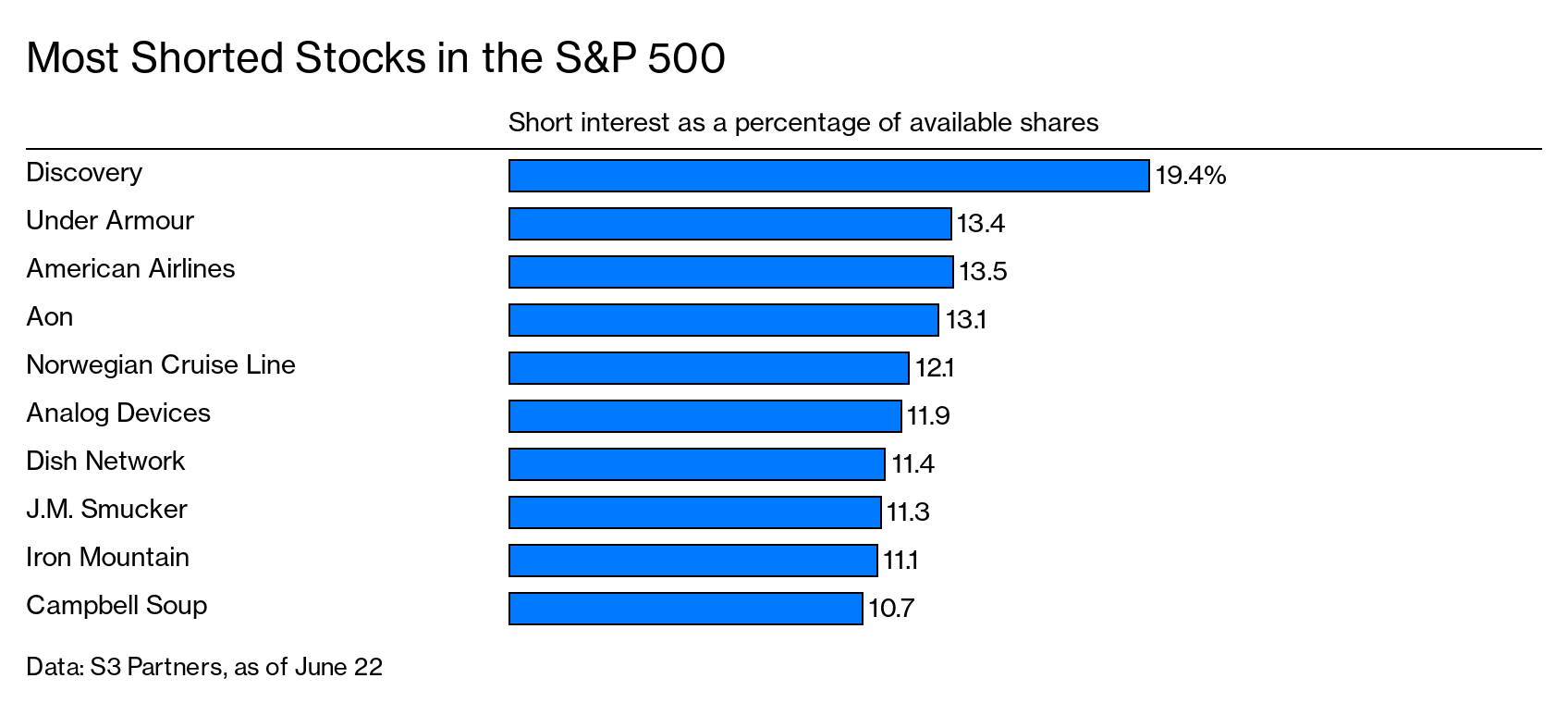

Most Shorted Stocks in the S&P 500

Data: S3 Partners, as of June 22

To see why, you need to understand the mechanics of shorting. Take GameStop as an example. Prior to its explosive jump in price early this year, hedge funds and other traders were arrayed against the video game retailer. That wasn’t crazy: Brick-and-mortar stores were hurting even before the pandemic, and GameStop’s main product is digital and increasingly sold over the internet. To short the stock, bears could borrow some shares—typically from a large money manager—and then sell them. Later they’d have to buy back the stock to return it to the owner. But if they were right and the shares fell, they could pocket the difference between the new price and the one they sold at. (Traders may also go short using options contracts.) In January, 140% of GameStop’s free-floating shares were tied to short sales. This can happen because a single share can be borrowed, sold, and then borrowed again from the new owner.

Because shorting puts a notch in the sell column for a stock, it can put pressure on its price to fall. So bulls naturally see shorts as working against them. The flip side is that the optimists can hurt the shorts—and even profit from doing so. A so-called short squeeze occurs when the price on a stock rises so much that shorts have to bail out of their trades. That means they have to buy back the shares they borrowed and sold, and their buying pushes prices even higher. The shocking upward spiral in GameStop shares in January appears to have been a squeeze. The more recent rally in the shares of cinema chain AMC could be an attempt to start one, as online influencers try to rally their troops against a common foe. Hedge funds trying to profit from the pain of an iconic business and its retail shareholders make for good villains.

Wall Street pros, on the other hand, tend to regard shorts as a necessary part of the financial landscape. They see financial markets not simply as a grocery store where you can buy things you want, but as a kind of machine for discovering correct prices. Shorts add an input—without them, the only people with a reason to have an opinion about a company would be people interested in buying or current owners thinking of getting out.

Shorting brings people who may be even harsher skeptics into the conversation. They don’t own the shares and don’t want to, but they still can signal that the stock’s overpriced—or that something isn’t quite right. They may even publicize their case against a stock and push its price down. “Short selling is generally a very positive thing for the market,” says Larry Tabb, head of market structure research at Bloomberg Intelligence. “It rewards people to provide information on what companies are saying and doing.”

Consider the case of Lordstown Motors Corp. and Hindenburg Research, which publishes online reports on stocks it might be shorting. Hindenburg issued a report in March alleging that Lordstown was making inaccurate statements. Chief Executive Officer Steve Burns and another executive abruptly left the company in June, and the board admitted some statements Lordstown had made were misleading, sending shares plummeting by more than 20% at one point. (Lordstown still denies most of Hindenburg’s specific allegations.)

Even more recently, shares of online sports betting company DraftKings Inc. were roiled after a critical report from Hindenburg. DraftKings has disputed Hindenburg’s claims, and said in a statement that the analysis “is written by someone who is short on DraftKings stock with an incentive to drive down the share price.” Hindenburg discloses in its report that it has a short position.

Critics of short sellers point out that their incentives are not simply a mirror image of buyers’ motivations. The potential upside for betting against a stock or bond is limited—a stock can only fall to $0—while losses are theoretically infinite if shares keep rising. So short sellers can’t just sit back, Warren Buffett-like, and wait for the world to agree with them. A fund that shorted GameStop in July 2020 at $3.85 could have made, at most, $3.85 a share minus borrowing costs. Anyone who took that position and stuck with it through June 21—an unlikely scenario—would be in the red a disastrous $196 for each share they shorted, plus expenses.

That asymmetry makes short selling like juggling chainsaws. And it helps fuel suspicions that some short sellers would be willing to do unscrupulous things to make sure they win, whether it’s manipulating markets behind the scenes or hyping up dubious cases against a company. On June 21, real estate company Farmland Partners Inc. said it settled litigation against Quinton Mathews, a short who published a pseudonymous blog post that led to a 39% decline in the stock. Mathews said in a statement that his article “contained inaccuracies and false allegations” and retracted it.

To be sure, plenty of big investors praise the shares they own, which may help their prices rise. You can see them every day on financial TV and quoted in the business news. But shorts may have an extra psychological edge they can exploit. According to a 2008 research paper published in the Psychological Bulletin, people have “the propensity to attend to, learn from, and use negative information far more than positive information.” In the context of investing, that means people may pay more attention to bearish news. Like it or not, a short seller peddling what bulls call FUD (or “fear, uncertainty, and doubt”) may resonate more than an optimist making the bull case.

Short sellers are a godsend for journalists. Because shorts think they have unique insights that haven’t been widely disseminated, they’re often willing to say things about a company that are spicier than the pablum found in your typical brokerage research report. That their quotes can be catchy makes it easy to write about them, which leads some people to think that reporters are in cahoots with the shorts. In practice, the outsize attention short sellers receive is mostly attributable to the fact that they’re often the only dissenting opinion to be found. Short sellers have helped reporters uncover frauds—the classic example is Enron Corp.—but they also take advantage of the news media’s deepest bias, which is for the interesting and salacious.

A dirtier way for shorts to game the system would be selling shares they haven’t actually borrowed, a practice known as “naked shorting.” In doing so, a short seller could place more pressure on the stock to go down than the market would naturally allow (because sometimes there just aren’t enough shares to borrow) while avoiding what can be hefty borrowing fees. The U.S. Securities and Exchange Commission banned naked shorting in 2008, but claims of its use were rampant on social media during GameStop’s first runup.

At the end of January, SEC data showed that $359 million of the company’s shares were deemed “failed-to-deliver.” That’s to say a big chunk of shares weren’t being handed over to buyers on time. That was seen by some on Reddit’s WallStreetBets forum as evidence of naked short selling, since you can’t deliver a stock you don’t have. Still, there are also more boring reasons, such as administrative delays, that may explain why shares can sometimes get caught in limbo, and the frenzy around GameStop shares may have made this more likely, too. “Fails-to-deliver can occur for a number of reasons on both long and short sales,” reads a

disclaimer on the SEC site. “Fails-to-deliver are not necessarily the result of short selling, and are not evidence of abusive short selling.”A more nuanced criticism of short selling is that it rubs up against the idea that investors should be long-term stewards of the businesses they own. Many shares are in the hands of mutual funds and pension funds that intend to hold them for years. Ironically, these are often the shares that shorts borrow to wager against a company.

For those big funds, lending shares provides a relatively safe stream of income from borrowing fees. But Japan’s Government Pension Investment Fund took an unlikely stand against the practice in 2019. Hiro Mizuno, then-chief investment officer of the $1.7 trillion fund, announced it would no longer lend its foreign shareholdings to short sellers, telling the Financial Times that he “never met a short seller who has a long-term perspective.” Lending shares can also undercut a large money manager’s efforts to encourage better environmental, social, and governance practices at companies. The Japanese pension fund’s strike at the short-selling complex elicited a thumbs-up at the time from Tesla Inc. CEO Elon Musk, who has infamously battled Tesla short sellers for years. He tweeted that the fund’s decision was the “right thing to do!” and that “short selling should be illegal.” After leaving GPIF, Mizuno joined Tesla’s board.

Regulators’ attitude toward short selling is that there are few problems transparency wouldn’t fix. When asked about his views at a May 6 hearing, SEC Chair Gary Gensler was cautious not to suggest he was in favor of any new strict limits on the practice. However, he indicated there may be a need for more disclosures and data about short positions.

Short selling is deeply dug into how money management works, because it’s not only for speculators. For fund managers, for example, a short bet can mitigate risks. Have a mandate to focus on airline stocks? Shorting hotel chains might ease any loss if airlines sell off because the two industries tend to move in the same direction.

Shorts are one-half of a free market’s checks and balances system, says Jacob Rappaport, head of equities at StoneX Financial Inc. Without them, valuations can become unhinged. “Voting with dollars and putting money to work shows conviction and helps the retail investor find true value,” he says. “Eliminating the mechanism to make a bearish investment does not make for a more efficient market.”

Read next:

Russell Index Rebalancing Brings Meme Stocks Into the Mainstream

"Short" - Google News

June 23, 2021 at 11:01AM

https://ift.tt/3gUxE7L

Reddit Hates Short Sellers, But the Stock Market Needs Them - Bloomberg

"Short" - Google News

https://ift.tt/2QJPxcA

Bagikan Berita Ini

0 Response to "Reddit Hates Short Sellers, But the Stock Market Needs Them - Bloomberg"

Post a Comment